Pick-N-Time’s Easy Financial Planning Routine includes the time, the procedures and the application to identify, record, forecast, evaluate, execute and review your basic personal financial data, plans and results.

This article, on the Easy Financial Planner (EFP) application is a robust, flexible, easy to use Microsoft Excel based application that serves as ‘Your Money GPS’. More than anything the Easy Financial Planner is as its name say, it is a planning tool which you can used to create and manage your basic financial plans (income, expenses, assets, and liabilities) one year at a time, by month.

The idea planning time, called Planning Season is October – December, for starting the following January 1st, after accounts are Updated.

The following are the major steps or procedures (instructions) for using the Easy Financial Planner:

- Three Name Lists (Oct): Income, Living & Debt Expense, Misc. Expense

- Name Manager (Oct): Setup with names from lists

- Profile (Oct-Nov): Identify and list all incomes and expenses—Get the Big Picture

- Initial Setup (Oct – Dec) Prepare annual plan across 12 monthly budgets

- (Jan 1st) – Update and verify all accounts (checking, escrow, saving, debt, etc.) balance.

- Compute & Record Jan 1st Net Worth

- Execution (Jan 1st– Dec 31st) -Start Jan Budget.

- Close Jan Budget

- Compute & Record Jan 31st Net Worth

- Start Feb Budget

- Close Feb Budget

- Compute Feb Net Worth (Last Day)

- Repeat Start, Close, Compute NW for each month

- Complete Next Year Profile & Setup (Oct-Dec)

- Close-Out Dec 31st

- Compute & Record December Net Worth

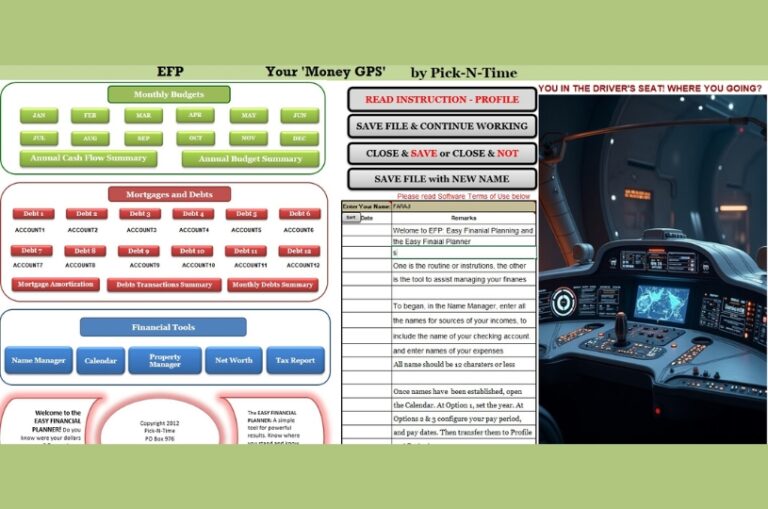

The following are the major parts or sections contained in the Easy Financial Planner application:

- Dashboard

- Commands Buttons

- Instructions Manuel (click ‘Read Instructions”)

- Notes and Reminders

- Profile (click ‘Read Instructions”)

- Name Worksheet* – use a sheet of paper.

- Monthly Budget Sections: Income, Living Expense, Mortgage & Debt, & Miscellaneous Expense

- Monthly Budget Section fields/columns: Name, Due Date, Budget Amt, Actual Amt, Clear Date, Variance

- Cashflow Summary: Income-Mortgage-Debt-Living Expense-Misc Expense=Balance

- Annual Budget Summary: Income, Date, Sum of Amt, Sum % of Amt. This tell where you money comes from and where it goes to & the percentage.

- Debt Registers: Record all charges, interest, refund and payments on loans and credit cards

- Mortgage Amortization Schedule: Setup and manage 2 mortgage and escrow accounts

- Debt Transactions Summary: For each Debt Register account, show total charges, interest, refunds and payment per month.

- Month Debt Summary – Display by month for all mortgage and debt register accounts the beginning balance, charges, interest, refunds, payments and ending balance.

- Calendar – Display pay days based on selected pay-period (weekly, semi-monthly, bi-weekly, monthly. Transfer pay dates to budgets.

- Name Manager—Add/Edit names for income, expenses, and account name selection on budget, Debt Register, Mortgage Amortization, Profile.

- Property Manager – Record your personal property of any value, for inclusion in Net Worth

- Net Worth Report –Summary of all assets, including home value and personal property, minus all liabilities, including mortgage balance and other debts.

- Tax Report – Shows items checked in budgets, or in debt register as tax deductible or tax significant.

To get started you need to gather all your financial documents i.e. contacts, subscriptions, pay stubs, utility and other account statements and, the names of assets, and liabilities. Some of this you will have in your mind. Start with all your existing or highly anticipated income and expenses, to make the lists below.

From these documents, you create 3 name lists, on a sheet of paper or in the Name Manager:

Incomes Living Expenses & Debt Expenses Miscellaneous Expenses

For each (income or expense) item, in each list, record a name, due date, and estimate budget amount.

Incomes Living & Debt Expenses Misc. Expenses

For example: My-Job 1/1/24 $1500 Electric 1/5/24 $75 Grocery 1/15/24 $73.12

Complete this for each income and each expense, including mortgages and other debts. Income name is the name of the source of any income deposited into your checking account. Living Expenses are scheduled expenses (you get a bill or know 30 days in advance, the amount &/or due date).

In the Miscellaneous Expense column, enter the name of businesses or places for your unscheduled expenses, such as groceries, auto fuel, fast food, which are un-schedulable, and made as needed. Misc. Expenses is more or less SPENDING money. Debt Expenses are the names of mortgage, auto loan, personal loan, and credit card companies. These names are stored in the same list, with Living Expense names. But only select them (credit & debt names) on the Profile or for a Mortgage Amortization Schedule or a Debt Register name. Once a name is selected for a MAS or Debt Register, that name will automatically appear on every budget. When Debt names are selected in the Profile, they transfer to the Debt Registers.

Complete the Initial Setup using Traditional Recording (Name, Due Date, Budget Amount). In each section, you can select income or expense name, enter due date and budget side amounts only. Later you will have the opportunity to implement Perpetual Recording, if you wish to use that method. Perpetual Recording allows you to use all the planning features and full capabilities of the app.

Some things, I find that make financial management, with the EFP easier: Go paperless and establish computer online access to all your financial accounts (bank, utilities, insurance, credit, etc.). Establish one checking for all deposits and payments. Make all regular incomes a direct deposit; put savings and utility expense on automatic payments or withdrawals from checking. Use budget or level utility payments. Ensure to automatically pay debts minimum payment a few days early. Always take your cash receipts, to record later. Go paperless on utilities and debts statements. View online or Download transactions and print, if needed, and use to update accounts in the EFP.

Establish an overdraft protection visa account, at your bank, linked to your checking account (visa/debit card). Use only to balance out payments, not as additional income. Always pay off overdraft amount, by end of month.

For expenses automatically paid, with a credit card, you can initially, while planning (Initial Setup) record them in the living expenses section, to see their impact on budgets. Then later remove and record in the appropriate debt register, when actually paid.

Secure a wireless or other printer, scanner & fax (some firms and gov’t agencies still use)

View or print out checking, debt or escrow account history from your bank, if need be, to reconcile accounts transactions to EFP’s budgets, or debt registers or escrow registers.

Your checking account is represented by the monthly budgets, in the EFP. When the current EFP budget is up to date, the balance should match your checking account balance.

Use Direct Deposit of income and automatic expense payments, as much as possible.

Frequently update all accounts: budget (checking), debt registers, including escrow inside Mortgage Amortization Schedule; update personal property in property manager; and update investments and savings accounts balance and real estate value, on Net Worth report. Always calculate and record the month’s ending net worth.

Traditional vs Perpetual Recording

Traditional Recording began by you, when performing the Initial Setup (planning). You enter in each section (Income, Living Expense, Debt Expense, Misc Expense) of the budget, enter a name, due date and budget amount. You then only enter an actual side amount, when the item is posted or clear checking. In other words, record the actual amount as they clear or post to checking–not before.

Perpetual Recording, unlike Traditional Recording, requires you to start with the planned amounts on both the budget and the actual side, in each section (incomes and all expenses) on all budgets. Each income and expense will show: Name, Due Date, Budget Amt, Actual Amt, Clear Date, Variance (0-zero).

Whether you use Traditional or Perpetual Recording, you must initially setup as to use Traditional Recording (Name, Due Date, Budget Amt) only. Then by executing a few other procedures (buttons) you can configure your plan for Perpetual Recording.

Perpetual Recording brings out the best of the EFP, turning it into a real planning tool, not just for seeing the balance of income minus expenses, as with Traditional Recording.

Color Coding (best use with Perpetual Recording, on the budgets or in debt registers )

The following color codes are applied to the ‘Clear Date’ of an Income or Expense transaction, to indicate the status of the income or a payment as follows:

Use black, blue, red or green (or your color choices) on the Clear Date (right click on date, pick color), to indicate:

Black-Initial setup–planned

Blue-Pending will post/clear checking in less than 5 days

Red-Due in greater than 5 days

Green-Cleared or posted to checking

Often when using Perpetual recording, and you have the actual side of the current budget up to date, which mean you must remove the actual side amount, of some uncleared transactions. But you may wish to simulate as if you have completed your plan for the whole year, (to see effect of completed and planned amounts) by completing the budget and actual side for all income and expenses transaction on all budgets, we have what can be called a ‘closed budget’, meaning every dollar has been accounting for—past income and expenses, and future income and expense. But some expenses will have cleared checking, some will be pending, and some due. Applying color code to distinguish. With a ‘closed budget’, you will have closed items and you have planned items, (in your budget—for checking account; but also, you can have (estimated) planned items (charges, interest, payments) in the Debt Registers, the payments of which transfer to the actual side of the budget (according to the payment date).

So, using Perpetual Recording, Color Coding, the Debt Registers, the Cashflow Summary, and the Monthly Deby Summary, you can record, monitor, analyze and do what-ifs to work your way out of debt, thereby increasing your financial wellbeing and eventually your net worth.

In summary, Easy Financial Planning was inspired by my mother’s rudimentary efforts to manage the little money she made as an uneducated field hand. She often wrote, on a small piece of brown grocery store bag, what little money she expected and bills due. On the flip side you made a list of items to get from grocery stores, things like soap and cleaning supplies. Most of our grocery food came in the form of commodities or government issued food to the poor—including that government cheese, so many remember. I have taken my mother’s efforts, converted it into a digital routine form, which has greatly helped me achieve goals and greatly improve my wealth profile.

Wealth doesn’t come by osmosis, wishing, hoping, etc., but usually by hard work or extra efforts, but most of all, by managing well what you got or will get.

Be Prosperous

FaraJi A.H. GoreDenna

Owner/Developer

Layton, UT 84040

www.pickntime.com

3 thoughts on “Pick-N-Time’s Easy Financial Planning Routine”

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.info/register-person?ref=IXBIAFVY

Your article helped me a lot, is there any more related content? Thanks!

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.